Contents

- 📊 Introduction to Emergency Funds

- 💸 Importance of Emergency Funds

- 📈 How to Calculate Your Emergency Fund

- 🏦 Where to Keep Your Emergency Fund

- 📊 Managing Your Emergency Fund

- 🚨 Common Mistakes to Avoid

- 📈 Emergency Fund and Investment

- 🤝 Emergency Fund and Credit Score

- 📊 Emergency Fund and Taxes

- 📈 Building an Emergency Fund from Scratch

- 📊 Maintaining and Updating Your Emergency Fund

- Frequently Asked Questions

- Related Topics

Overview

An emergency fund is a pool of savings set aside to cover unexpected expenses, such as car repairs, medical bills, or losing a job. Historian David Bach notes that the concept of emergency funds dates back to ancient civilizations, where people would store grain and other essentials in case of famine or war. However, skeptic Helaine Olen questions whether the traditional three-to-six-month rule of thumb is sufficient, given the rising costs of living and the increasing frequency of financial shocks. According to a 2020 survey by the Federal Reserve, 39% of Americans couldn't cover a $400 emergency expense, highlighting the need for a more robust safety net. Engineer and financial expert, Farnoosh Torabi, recommends automating emergency savings and exploring alternative funding sources, such as crowdfunding or community-based lending. As the futurist, Yuval Noah Harari, notes, the rise of the gig economy and AI-driven job displacement may require a fundamental rethink of our approach to emergency funding, with some experts advocating for a universal basic income or other forms of social protection.

📊 Introduction to Emergency Funds

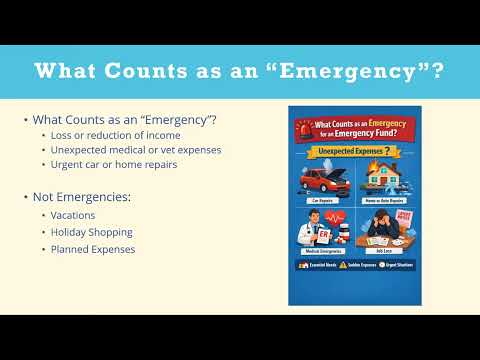

An emergency fund, also known as a contingency fund, is a personal budget set aside as a financial safety net for future mishaps or unexpected expenses. A critical part of financial planning, it is supposed to ensure one's personal finances are prepared for any emergency so that the risks of becoming dependent on credit, falling into debt, or running out of money in general are reduced if such a situation were to occur. According to financial planning experts, having an emergency fund in place can provide peace of mind and reduce financial stress. It's essential to understand the importance of emergency funds and how they can help in times of need. For instance, an emergency fund can help cover unexpected medical expenses, car repairs, or unemployment benefits.

💸 Importance of Emergency Funds

The importance of emergency funds cannot be overstated. It's a crucial component of personal finance that can help individuals and families navigate unexpected expenses and financial setbacks. Without an emergency fund, people may be forced to rely on high-interest credit cards or payday loans, which can lead to a cycle of debt and financial hardship. On the other hand, having a well-funded emergency account can provide a sense of security and reduce the risk of financial difficulties. As noted by Dave Ramsey, a well-known personal finance expert, an emergency fund should cover at least 3-6 months of living expenses. It's also essential to consider inflation and emergency fund investment options to ensure the fund grows over time.

📈 How to Calculate Your Emergency Fund

Calculating your emergency fund requires considering several factors, including your income, expenses, debts, and financial goals. A general rule of thumb is to save 3-6 months' worth of living expenses in an easily accessible savings account. However, this amount may vary depending on individual circumstances, such as job security, health insurance, and dependent care. It's also essential to consider emergency fund withdrawal strategies and tax implications to ensure you're making the most of your emergency fund. For example, you may want to consider tax-advantaged accounts such as a high-yield savings account or a money market fund.

🏦 Where to Keep Your Emergency Fund

When it comes to where to keep your emergency fund, it's essential to choose a safe and easily accessible location. A high-yield savings account or a money market fund are popular options, as they offer competitive interest rates and low risk. It's also crucial to consider liquidity and emergency fund access to ensure you can quickly access your funds in case of an emergency. As recommended by Suze Orman, a well-known personal finance expert, it's essential to keep your emergency fund separate from your everyday spending money to avoid the temptation to dip into it for non-essential expenses. You may also want to consider budgeting apps to help you track your expenses and stay on top of your emergency fund.

📊 Managing Your Emergency Fund

Managing your emergency fund requires regular monitoring and adjustments to ensure it remains adequate and aligned with your changing financial circumstances. It's essential to review your emergency fund regularly and make adjustments as needed to reflect changes in your income, expenses, or financial goals. You may also want to consider emergency fund rebalancing to ensure your fund remains optimized and aligned with your investment objectives. As noted by Jean Chatzky, a personal finance expert, it's also crucial to consider inflation and interest rates when managing your emergency fund to ensure it keeps pace with the rising cost of living. You may also want to explore retirement planning options to ensure a secure financial future.

🚨 Common Mistakes to Avoid

Common mistakes to avoid when it comes to emergency funds include failing to prioritize saving, not having a clear understanding of your expenses, and not considering inflation or interest rates. It's also essential to avoid dipping into your emergency fund for non-essential expenses, such as vacations or hobbies. As warned by David Bach, a personal finance expert, raiding your emergency fund can lead to a cycle of debt and financial hardship. Instead, focus on building a stable emergency fund and exploring investment options to grow your wealth over time. You may also want to consider credit counseling to help you manage your debt and improve your credit score.

📈 Emergency Fund and Investment

When it comes to emergency funds and investment, it's essential to consider low-risk investment options that align with your financial goals and risk tolerance. A high-yield savings account or a money market fund are popular options, as they offer competitive interest rates and low risk. However, it's also important to consider inflation and interest rates to ensure your emergency fund keeps pace with the rising cost of living. As recommended by Burton Malkiel, a personal finance expert, it's essential to diversify your investments and consider tax-advantaged accounts to optimize your returns. You may also want to explore ROTH IRA or 401k options to save for retirement.

🤝 Emergency Fund and Credit Score

An emergency fund can also have a positive impact on your credit score. By having a stable emergency fund in place, you can reduce the risk of missing payments or accumulating debt, which can negatively impact your credit score. As noted by FICO, a leading credit score provider, having a stable emergency fund can demonstrate responsible financial behavior and improve your creditworthiness. It's also essential to consider credit monitoring and identity theft protection to ensure your financial information remains secure. You may also want to explore credit card rewards to earn points or cashback on your purchases.

📊 Emergency Fund and Taxes

When it comes to emergency funds and taxes, it's essential to consider the tax implications of your emergency fund. A tax-advantaged account such as a high-yield savings account or a money market fund can help minimize taxes and optimize your returns. As recommended by TurboTax, a leading tax preparation software, it's essential to consider tax deductions and tax credits to reduce your tax liability. You may also want to explore tax planning options to ensure you're taking advantage of available tax savings opportunities.

📈 Building an Emergency Fund from Scratch

Building an emergency fund from scratch requires discipline and patience. It's essential to start by setting a realistic goal, such as saving $1,000 or 3-6 months' worth of living expenses. As recommended by The Balance, a leading personal finance website, it's essential to create a budget and track your expenses to identify areas where you can cut back and allocate funds to your emergency fund. You may also want to consider budgeting apps or spreadsheets to help you stay on track and monitor your progress.

📊 Maintaining and Updating Your Emergency Fund

Maintaining and updating your emergency fund requires regular monitoring and adjustments to ensure it remains adequate and aligned with your changing financial circumstances. It's essential to review your emergency fund regularly and make adjustments as needed to reflect changes in your income, expenses, or financial goals. As noted by Kiplinger, a leading personal finance magazine, it's also crucial to consider inflation and interest rates when managing your emergency fund to ensure it keeps pace with the rising cost of living. You may also want to explore retirement planning options to ensure a secure financial future.

Key Facts

- Year

- 2020

- Origin

- Ancient Civilizations

- Category

- Personal Finance

- Type

- Financial Concept

Frequently Asked Questions

What is an emergency fund?

An emergency fund, also known as a contingency fund, is a personal budget set aside as a financial safety net for future mishaps or unexpected expenses. It's a critical part of financial planning that can help individuals and families navigate unexpected expenses and financial setbacks. According to financial planning experts, having an emergency fund in place can provide peace of mind and reduce financial stress. You may also want to consider budgeting apps to help you track your expenses and stay on top of your emergency fund.

How much should I save in my emergency fund?

A general rule of thumb is to save 3-6 months' worth of living expenses in an easily accessible savings account. However, this amount may vary depending on individual circumstances, such as job security, health insurance, and dependent care. It's also essential to consider inflation and interest rates to ensure your emergency fund keeps pace with the rising cost of living. As recommended by Dave Ramsey, a well-known personal finance expert, an emergency fund should cover at least 3-6 months of living expenses.

Where should I keep my emergency fund?

A high-yield savings account or a money market fund are popular options, as they offer competitive interest rates and low risk. It's also crucial to consider liquidity and emergency fund access to ensure you can quickly access your funds in case of an emergency. As recommended by Suze Orman, a well-known personal finance expert, it's essential to keep your emergency fund separate from your everyday spending money to avoid the temptation to dip into it for non-essential expenses.

Can I use my emergency fund for non-essential expenses?

No, it's essential to avoid dipping into your emergency fund for non-essential expenses, such as vacations or hobbies. As warned by David Bach, a personal finance expert, raiding your emergency fund can lead to a cycle of debt and financial hardship. Instead, focus on building a stable emergency fund and exploring investment options to grow your wealth over time. You may also want to consider credit counseling to help you manage your debt and improve your credit score.

How often should I review my emergency fund?

It's essential to review your emergency fund regularly, such as every 6-12 months, to ensure it remains adequate and aligned with your changing financial circumstances. As noted by Kiplinger, a leading personal finance magazine, it's also crucial to consider inflation and interest rates when managing your emergency fund to ensure it keeps pace with the rising cost of living. You may also want to explore retirement planning options to ensure a secure financial future.

Can I use my emergency fund for retirement expenses?

No, it's essential to keep your emergency fund separate from your retirement savings. As recommended by Charles Schwab, a leading investment management company, it's essential to prioritize retirement savings and explore retirement planning options, such as a 401k or an IRA, to ensure a secure financial future. You may also want to consider tax-advantaged accounts to optimize your returns and minimize taxes.

How can I build an emergency fund from scratch?

Building an emergency fund from scratch requires discipline and patience. It's essential to start by setting a realistic goal, such as saving $1,000 or 3-6 months' worth of living expenses. As recommended by The Balance, a leading personal finance website, it's essential to create a budget and track your expenses to identify areas where you can cut back and allocate funds to your emergency fund. You may also want to consider budgeting apps or spreadsheets to help you stay on track and monitor your progress.